About Me

CS PhD Candidate @ Sapienza

AI Scientist @ Outsampler

I am an AI Scientist at Outsampler, crafting research and innovation at the intersection of artificial intelligence and finance.

I am also a dedicated PhD candidate in Computer Science at Sapienza, University of Rome. My research focuses on Artificial Intelligence for Finance, including generative modeling and causal discovery in time series data.

With a strong background in both theoretical computer science and practical software development, I am passionate about bridging the gap between academic research and real-world applications. My work has been published in several peer-reviewed journals and presented at international conferences.

Resume

Education

Thesis: "Adversarial Learning to Rank - Transferable Text-Based Attacks to Black-Box Neural Ranking Models: WARA and WSRA"

Thesis: "Diffusion in the Presence of Ambivalent relationships: The Role of the Negative relationships in the complexity of the Problem"

Experience

Skills

Publications

Projects

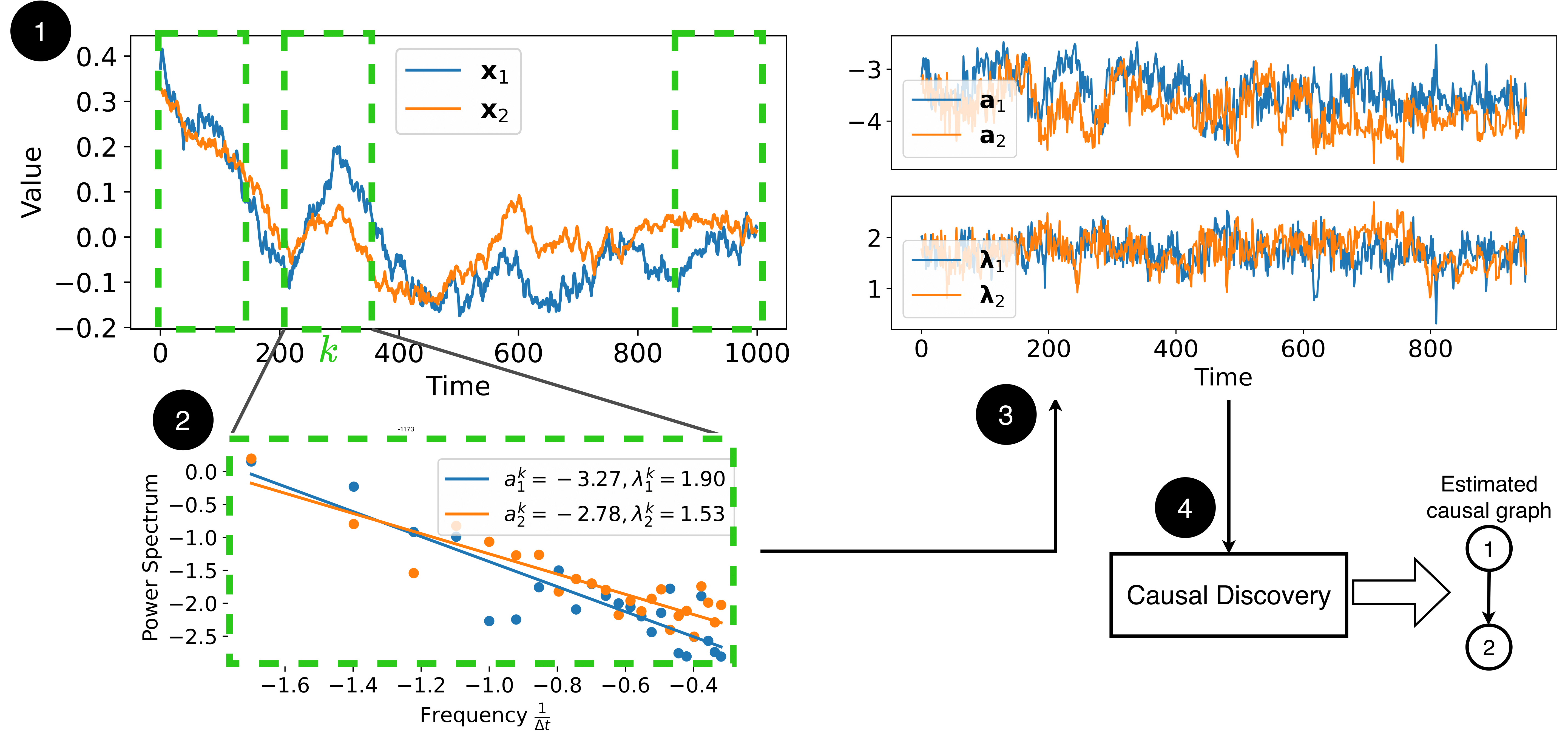

PLACy

Robust causal discovery method for stochastic time series leveraging power-law spectral features. Exploits the inherent power-law distribution in real-world time series frequency spectra to amplify genuine causal signals and reduce noise sensitivity, outperforming state-of-the-art alternatives on synthetic and real-world datasets.

LOBCAST

Open-source Python framework for Stock Price Trend Prediction (SPTP) standardization, implementing data preprocessing, deep learning model training, evaluation, and profit analysis. Benchmarks fifteen state-of-the-art deep learning models on Limit Order Book data, examining robustness and generalizability.

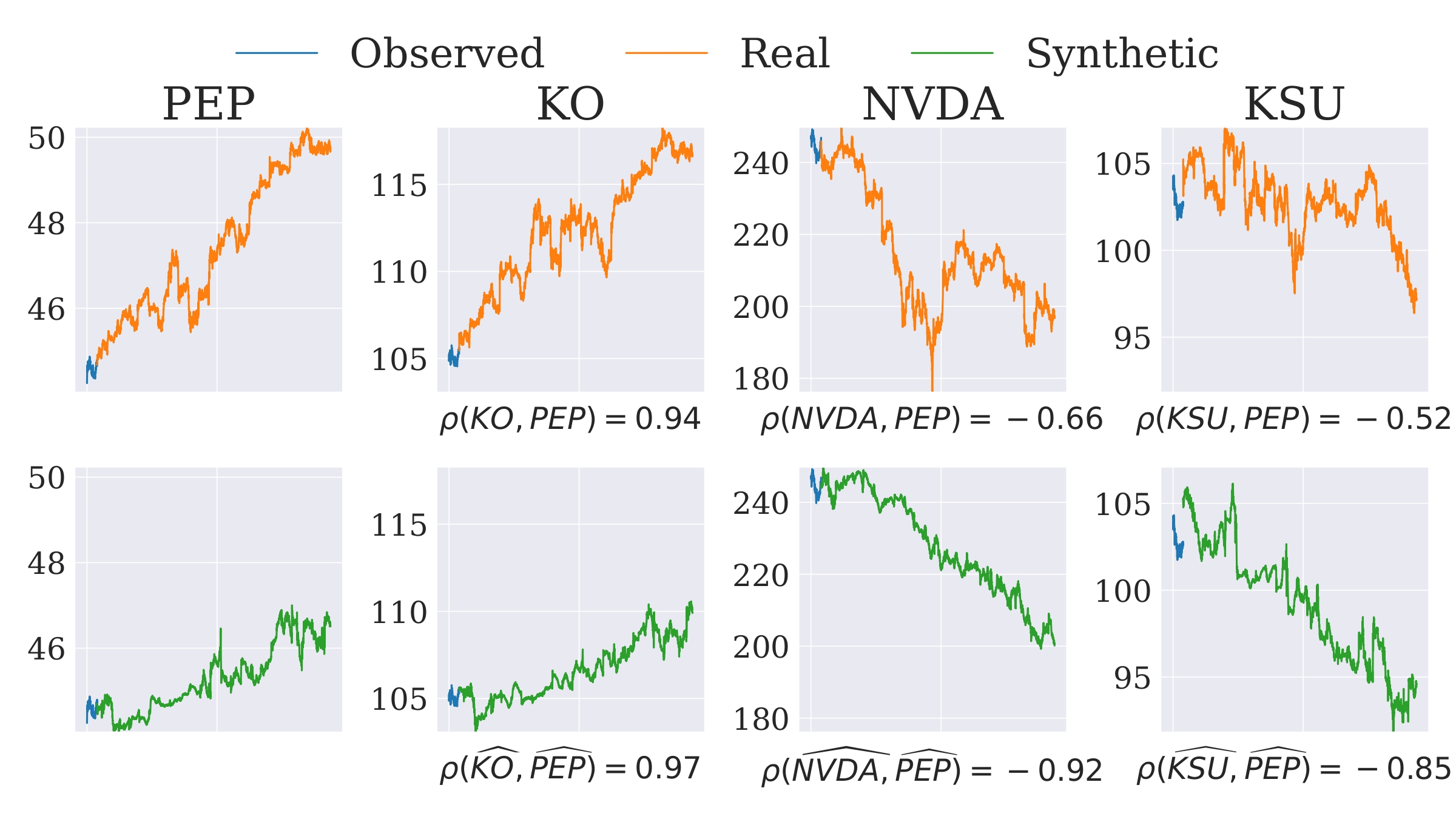

CoMeTS-GAN

Correlated Multivariate Time Series generative framework based on Conditional Generative Adversarial Networks (C-GANs) designed to generate price and volume time series of correlated stocks. Accurately learns and reproduces stylised facts and inter-asset correlations, crucial for achieving realism in multi-stock simulation environments.

Stock Shocks Modelling and Forecasting

Formal definition of stock shocks based on fat-tailed Lévy-stable distributions. Implemented forecasting algorithms using Limit Order-Book data with machine learning approaches (random forest, hierarchical clustering) achieving high precision and recall.

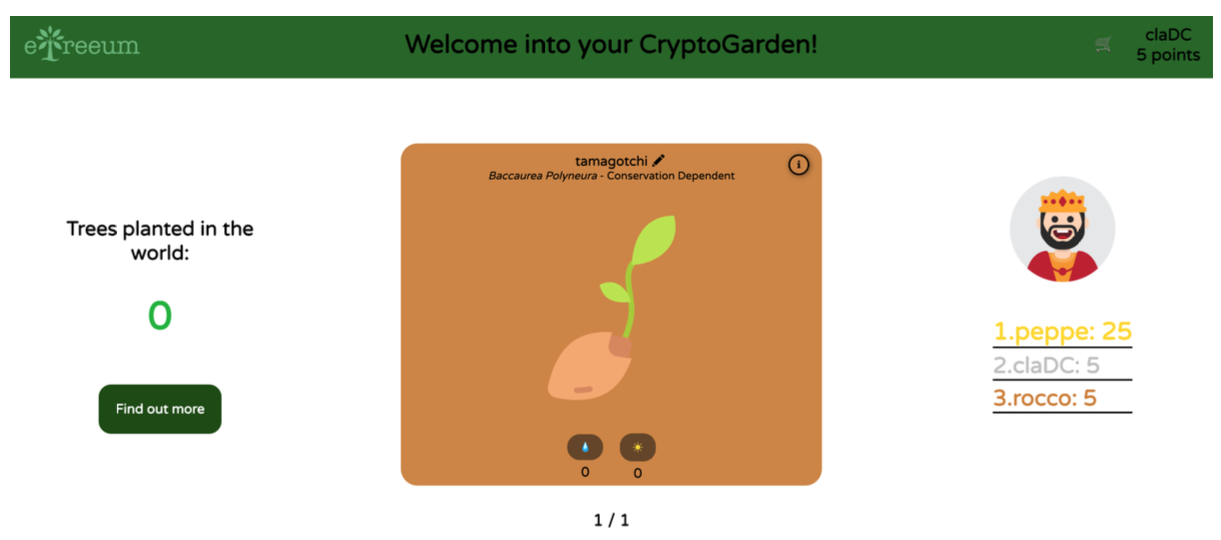

eTreeum

eTreeum was created to help raise awareness on the environmental impact of blockchain technologies. Ideally, users of this app will help plant trees in the real world by playing with crypto-trees. Users are able to start with a free seed, take care of it and then sell it for cryptocurrencies.